Spanish Hotel Market 2024

- May 30, 2024

- 6 min read

Updated: Apr 30, 2025

SPAIN’S TOURISM SECTOR in 2023 exceeded all initial expectations and surpassed the high levels achieved in the 2019 season before the pandemic, both in nominal expenditure and real terms. This achievement is particularly remarkable considering the context of high inflation, with tourism prices nearly 18% higher than in 2019.

The positive trend is projected to continue through 2024, with the tourism industry expected to outpace the overall economy’s growth. According to the OECD, the industry’s GDP is forecasted to grow by 2.5%, while the overall economy is expected to increase by 1.8%. In 2023, the tourism industry made a significant contribution of 12.8% to the GDP and accounted for 12.6% of the total workforce.

In 2023, there was a 1.9% increase in overnight stays compared to 2019. This growth can be attributed to two main factors: the resilience of domestic tourism, which saw a 5.5% increase, and the recovery of international tourism, with 85.2 million international visitors in 2023 compared to 83.5 million in 2019. Although the British market (the main feeder market for Spain’s tourism) is not still at the pre-pandemic levels on a full-year basis, the last quarter of 2023 exceeded the 2019 figures, which gives room for optimism.

The comparison to the end of fiscal year 2019 proves to be insightful, as it remains the most successful historical fiscal year in the hotel industry. Despite the 7.4% growth in occupancy in 2023 compared to 2022, reaching 72.8%, it still falls short by almost 3% when compared to the 2019 figure of 74.7%. Conversely, both ADR and RevPAR have surpassed the 2019 numbers. The ADR of €144.5 in 2023 is 22% higher than the €118.4 in 2019, while the RevPAR has also increased from €88.5 in 2019 to €105.1 in 2023, marking an 18.7% rise.

The gathered data validates the positive advancement of hotel and tourism operations across all locations, albeit with more substantial expansion observed in major urban centres compared to coastal and resort destinations. This discrepancy can be attributed, in part, to the fact that 2022 had already been a remarkable year for the latter.

Spanish Hotels Performance 2023 VS 2022

Spanish Hotels Performance 2023 VS 2022

Hotel investment and main transactions

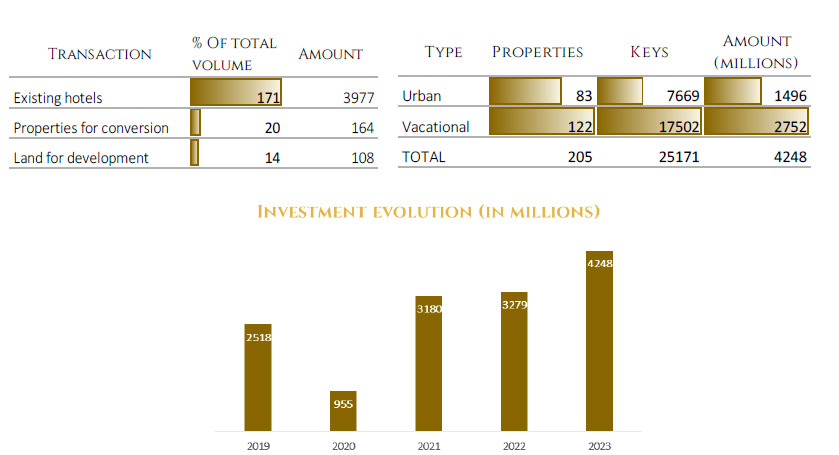

In 2023, the hotel investment volume in Spain reached €4.2 billion (36% of the total investment in the country and the only real estate segment with an increase compared to 2022), considering existing hotels, properties for conversion to hotel use, and land for development. During the year, a total of 205 assets were transferred, compared to 163 in 2022. After overcoming the barrier of €3 billion, 2023 beat all forecasts, ranking only behind 2018 -the year when Blackstone took over the Socimi Hispania in a transaction that valued its hotel portfolio at €2 billion.

Transactions and volume

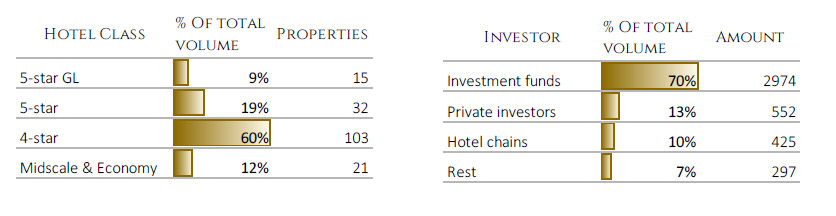

There was a notable rise in hotel asset transfers in 2023, with 171 hotels and more than 21,000 rooms changing ownership, compared to 158 hotels and 18,000 rooms in 2022 (the total Spanish market accounted for 1533 thousand beds and 14426 hotels in 2023). High-end hotels are particularly interesting to investors due to their consistent demand, comprising 85% of all transactions. Remarkably, 11 major hotel portfolios contributed to 64% of the total volume (2.6 billion euros) in 2023.

The primary investor profile was investment funds (with a remarkable presence of sovereign funds), representing over 70% of the total volume. Private investors comprised 13%, while hotel chains accounted for 10%. The primary source of capital came from international buyers, particularly from Saudi Arabia, UAE, and Singapore, constituting more than 75%.

The acquisition of the Mandarin Oriental Barcelona by the Saudi fund The Olayan Group, which is also a co-owner of the Mandarin Oriental Ritz Madrid, has garnered significant attention. This transaction has been valued at over €200 million.

Transaction by asset type and investor profile

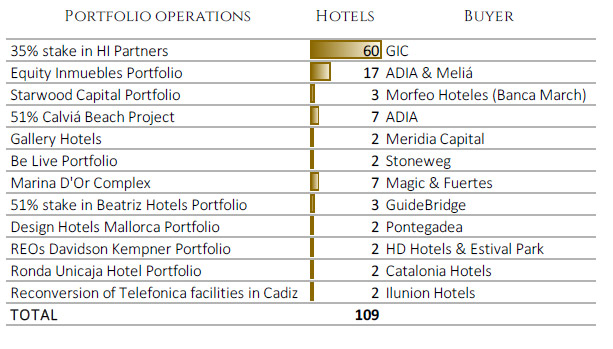

Singapore’s sovereign wealth fund GIC made a significant move this year by acquiring a 35% stake in HI Partners, a Blackstone hotel investment vehicle. This investment follows GIC’s recent purchase of a majority stake in the Sani chain Ikos Resorts, which was the largest hotel deal of 2022. GIC is showcasing its strong dedication to the hospitality industry by venturing into the Mediterranean holiday hotel sector. HI Partners, boasting a portfolio of 73 operational hotels and ownership of over 50 properties in Spain, including those in the Canary Islands and the Balearic Islands, holds a prominent position in the European tourism market. This strategic investment will bolster the fund’s assets and expand its footprint in Southern Europe.

Portfolio operations in 2023

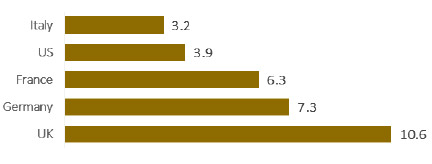

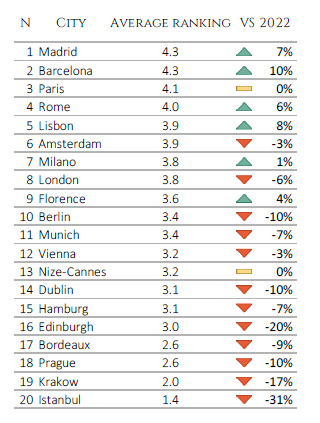

Madrid and Barcelona emerged as the top two cities for European investment in 2024, according to a study conducted through 60 interviews with executives. The research compiles the perspectives of companies that represent a combined total of 18 billion euros in hotel investments between 2019 and 2023.

Albert Grau, partner and co-director of Cushman & Wakefield Hospitality in Spain, “the position of Spain and the entire Iberian Peninsula continues to attract investment thanks to the attractiveness and solidity of the destination, both urban and vacation. Although prices are already at healthy levels, there is still potential for revaluation and profitability in line with what investors are looking for. In vacation destinations, we can see more value-added investment opportunities in second- and third-line beach locations for product repositioning, while in urban areas, more trophy assets or conversion opportunities from other uses to hotels are sought in cities where regulations allow it.”

Top 20 most attractive European cities for hotel investment

Spanish market structure

In the past, and until quite recently, the industry was primarily defined by the prevalence of family-owned businesses (such as Meliá, Iberostar, Barceló, and Riu) that originated in Spain during the 1950s and 1960s. These companies then expanded into other markets and are currently managed by the second or third generations.

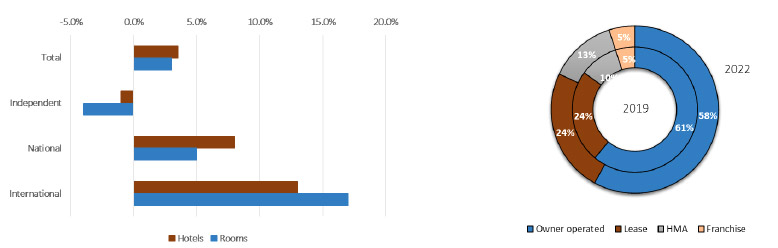

However, Spain’s appeal as a tourist destination has encouraged foreign hotel groups to focus their growth on the country, alongside the entry of new investment funds (currently the main type of investor). Spain is in the process of constant professionalization and adaptation to new management formulas. With a hotel supply still dominated by independent hotels, Spain offers many opportunities for the arrival of new hotel brands. 4-star hotels still hold the majority share in the market, but the 5-star category experienced the highest growth (+12% in rooms) primarily due to the presence of international groups.

Despite the dominance of owner-operated hotels (58% in rooms from hotel groups), there has been significant growth in management and franchise contracts (+31% and +10%, respectively), indicating the preference of international groups for such agreements. Half of Spain’s hotel room supply comes from owner-operated hotels, which presents a substantial opportunity for international hotel companies to transform this supply into branded hotels. In the last years, 11 new hotel groups have entered Spain, including Four Seasons and Rosewood.

66% of the rooms incorporated are part of the resort segment, totalling 14,904 rooms. On the other hand, the urban segment accounts for 34% of the rooms, amounting to 7,736 rooms. Despite the popularity of coastal areas, major international luxury hotel chains focus on big cities like Madrid (Four Seasons and Rosewood), Seville, Barcelona, and Bilbao (Radisson). Additionally, secondary destinations are now catching the eye of budget hotel brands such as Ibis (Accor), HIEX (IHG), and B&B in cities like Lugo, Girona, Logroño, Mataró, and Sant Cugat.

2019 vs. 2022 variation

Looking forward to the future

Although the complete recovery from the pandemic will normalize growth rates in the coming years, the recovery of purchasing power in Spain and Europe and Spain’s greater geopolitical stability in relation to the competing countries will boost the tourism sector to new records in 2024.

Anticipated growth is projected in both the number of travelers and overnight stays. It is forecasted that there will be 113.8 million travelers, representing a 1.6% increase from 2023, and 352 million overnight stays, a 1.5% increase from the previous year. Foreign tourism is expected to exhibit even more significant growth, with a projected increase of 2.5% compared to 2023.

There are predictions of a modest 2.3% increase in the ADR by 2024 compared to the previous year. Despite this slower growth rate, occupancy values are expected to remain stable, with a slight increase of 1.1% compared to 2023 after reaching pre-pandemic levels. The RevPar is projected to rise by 3.4% from 2023, reaching 81.7 euros by the end of 2024. Looking ahead to 2025, there are forecasts of slightly higher ADR increases, averaging at 3% annually.