In the Pacific, we now provide asset management for the InterContinental Wadra Bayin Lifou, New Caledonia. In the GCC, we added more than 10 luxury hotels under asset management in 2023, including a Ritz Carlton, W Hotel, JW Marriott, Nikki Beach and InterContinental hotel. In Europe, we have renewed our collaboration with luxury hotels under operation, e.g., with Accor or Four Seasons.

We have also bolstered our team worldwide with the addition of Lionel Anidjar and David Boveda, who bring decades of hotel experience into the fold.

These are thrilling times. The hotels we work with are at the forefront of innovation, creating memorable guest experiences and peak value and performance for investors. Demand for independent asset management is growing.

As we enter the new year, we look forward to change and consolidation in this sector we are proud to call home.

Global Asset Solutions on the road

We will be sponsoring HOFTEL’s AOHIS event in January in Madrid, where CEO Alex Sogno will be chairing the panel GOPAM(GOP per sqm) – is F&B really a problem, or a hidden gem? on Tuesday 23rd. Alex will be joined onstage by Nils Scheers, Chief Operating Officer, Thynk.Cloud, Michael Grove, Chief Operating Officer, HotStats and Miguel Casas, Managing Director, Stoneweg Hospitality.

Robert Walters, Chief Investment Officer, will join Alex at the event. We hope to see you there.

F&B to fill your balance sheet

Ahead of Alex’s panel, we discuss how to make your F&B – whisper it – profitable.

F&B is usually the second-highest profit driver in the hotel after the rooms. Nevertheless, its margin is not always as high as the rooms due to the nature of the business with high fixed costs. It is usually divided into two categories: the banqueting and the other outlets such as restaurant, bar and room service.

Everywhere, except maybe in the Middle East and Asia, the clients are not used to associating a good meal with a hotel restaurant. This sometimes resulted in neglect of the restaurants when discussing the CapEx. In contrast, restaurants worldwide have become hives of innovation, with foam and moss and foraging firing guests’ imaginations.

To read more, click here.

Bringing strength to soft brands

‘Another day, another brand’ could well be the catchphrase of our sector, but as with everything in this industry we call home-from-home, it’s never as simple as that. The past couple of decades have seen a rapid evolution away from the owner/operator model, which has kept the sector tick-ing along for thousands of years, and we’d all be forgiven for feeling dizzy from the shift.

The large brand stables have quickly jettisoned their hotel ownership and, with it, many of the re-sponsibilities. After the big shareholder payday, which resulted from selling off their assets, the majority are focused on a fee-based model, which, for the small companies in particular, can pre-sent valuation challenges on the open markets.

To read more, click here.

When faced with complexity, try creativity

Switzerland is justly famous for many things; from stunning natural beauty to watches and diplomacy, but perhaps most notably are their banks. Inscrutable, discrete and going about their business for centuries with a watchful eye over both profit and risk. Perhaps coincidentally, another great Swiss icon is the eponymous multi-faceted Army Knife; an item noted for versatility and adaptability.

When debt is readily available, the borrowing process can be straightforward. When times get tough and the shutters come down, however, borrowers need to work harder to secure the debt they need. To use an analogy, faced with such challenges, it can pay to consider those attributes associated with the Swiss Army Knife. You need to use every tool at your disposal to prize every pound, dollar or euro from your balance sheet to impress a lender and stress upon them that you are a satisfactory risk. It can also pay to approach the process with a degree of creativity.

To read the full article, as published by GRI Europe, click here.

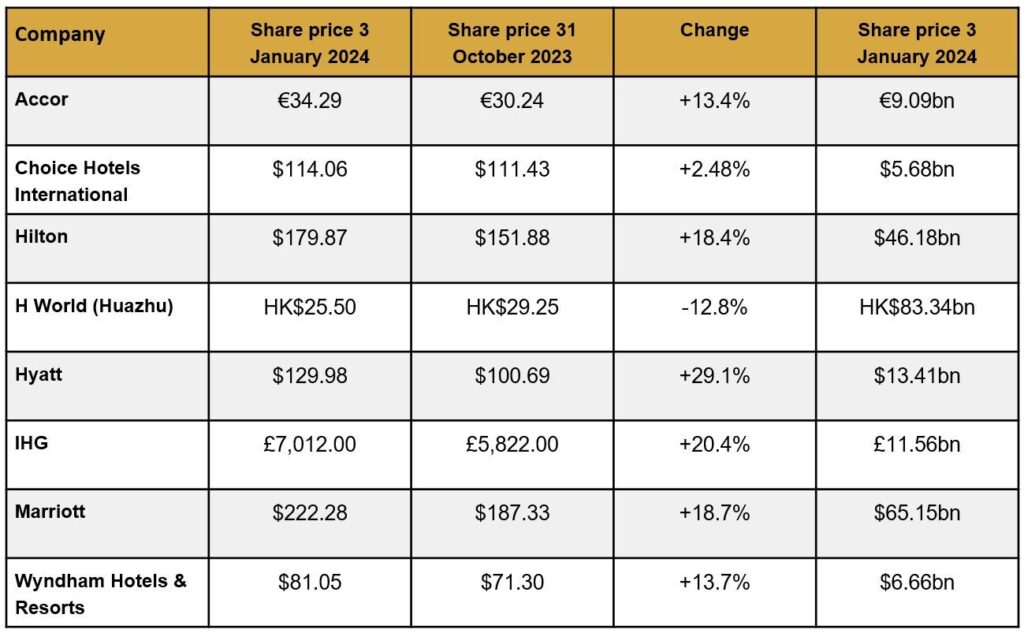

The sector in numbers

The hotel sector saw a strikingly strong close to the year, as performance continued to grow and forecasts for 2024 suggested that the industry would enjoy continued revpar growth into the new year as room rates remained strong.

The potential for large deals in the market held investors’ interest and drove speculation, aided by the ongoing machinations involved with Wyndham and Choice. At the time of writing, Wyndham continued resisting Choice’s approaches. Still, the latter was throwing all it had at the potential deal, claiming that many Wyndham shareholders were supportive of the takeover.

The saga looks set to run long into 2024, with reports in Reuters suggesting that Choice had been acquiring Wyndham shares with a view to nominating board members and pursuing the move from the inside.

Elsewhere in the industry, ongoing speculation around what Accor might do this year regarding a split was supporting its share price. At the same time, analysts pointed to a return to more recog-nisable work patterns which would favour hotels over Airbnb as digital nomads fell away.

All the signs are pointing to a good year for the hotel sector, and with more mainstream investing heading into it, demand for asset management has never been higher